Perhaps the best-known stock market index in the world, the benchmark Dow Jones Industrial Average, underwent a makeover last week to reflect emerging market realities.

As Ms Kristina Hooper, chief global market strategist at Invesco, was quoted as saying: Old economy component stocks were replaced by new economy stocks.

Essentially the rebalancing or rejigging saw petrochemical giant ExxonMobil, pharmaceutical firm Pfizer and aerospace-defence player Raytheon replaced on the 30-stock index by cloud computing specialist Salesforce, biotech firm Amgen, and aerospace and industrial manufacturing company Honeywell International.

A key reason for the rebalancing was the impending four-to-one split of Apple stock today that would effectively reduce the tech sector's representation on the price-weighted Dow index.

But as S&P Dow Jones Indices, the company which oversees the Dow, said, the rebalancing was also to diversify the index by removing overlaps between companies of similar scope and adding new types of businesses that better reflect the American economy.

Indeed, the evolution of the United States economy has seen many older giants, like General Electric and ExxonMobil, being replaced on Wall Street's main indexes by the likes of Facebook, Apple, Amazon, Alphabet, Netflix and Google (collectively known as Faang).

There is an important lesson here for Singapore, and in particular the market's benchmark FTSE Straits Times Index, commonly known as the STI. The STI was set up in 1966, and during its first 30 years it mirrored the economic transformation of Singapore from a Third World to First World country.

The Britain-based FTSE Russell partners with Singapore Press Holdings (SPH), publisher of The Straits Times, and the Singapore Exchange to jointly compute and manage the avatar of the benchmark indicator of the Singapore stock market.

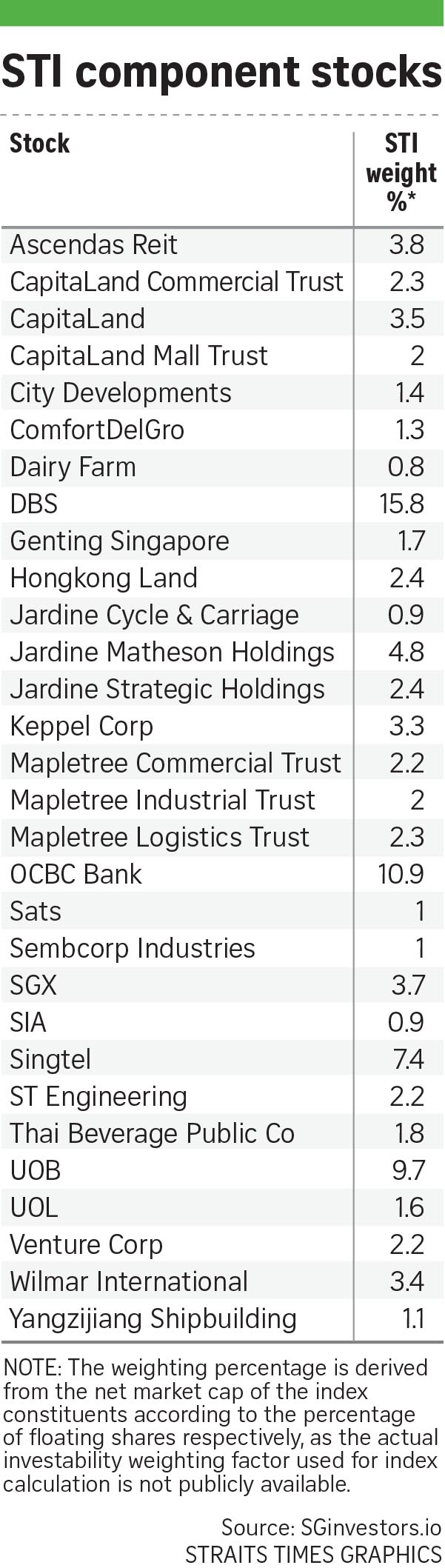

Like the Dow, the Singapore index comprises 30 component stocks of the largest listed companies, subject to free float and liquidity criteria.

These include the three local banks, six real estate investment trusts, prominent Temasek-linked players like Singtel, Singapore Airlines, Sembcorp Industries and ST Engineering, a handful of property companies, the Singapore Exchange, ComfortDelGro and a few others.

There are seven "foreign" companies, comprising the likes of the Jardine group, Yangzijiang Shipbuilding Holdings and Thai Beverage.

The only company that comes anywhere close to being a "tech" play is home-grown contract manufacturer Venture Corp.

There are periodic reviews of the index, leading to tweaks and rebalancings. A major one was done in September 2015, when UOL Group, Yangzijiang and Sats replaced Jardine Matheson Holdings, Jardine Strategic Holdings and Olam International as constituents following a semi-annual review. Both Jardine companies rejoined the index later.

More recently, the index went through a minor rejig in June when Mapletree Industrial Trust was added and SPH removed.

The five highest-ranking non-constituents of the STI by market capitalisation - Keppel DC Reit, Suntec Reit, NetLink NBN Trust, Frasers Logistics and Industrial Trust, and Keppel Reit - were added to the STI reserve list, ready to replace any constituents that become ineligible as a result of corporate actions, before the next review. Another review is due on Thursday.

But there has been a lot of debate about how well the STI represents the underlying market and the Singapore economy.

Granted that index construction is not an exact science; there have to be judgment calls in the case of stocks that meet the liquidity and size requirements on paper, but may suffer from poor governance or have "reputational" issues.

But there are some shortfalls in the existing composition of the index that must be addressed.

First is the glaring absence of tech plays.

While Singapore is no Wall Street and we do not have the big "Faang-type" plays here, surely we have enough listed companies associated with, and supporting, the big techs of the world?

Should they not get some recognition on the Singapore benchmark index?

Secondly, the three banks - DBS Bank, United Overseas Bank and OCBC Bank - comprise 36 per cent of the weighting of the index. By any reckoning, this is an "overweight" of a single sector.

On the subject of overweight, five of the component companies comprise 50 per cent of the net market cap of the 30 companies in the index.

Also, there are 640 mainboard and 215 Catalist listings. Yet the STI components comprise only 5 per cent of the companies listed on the mainboard. So the index does seem somewhat of a narrow reflection of the broader market.

Finally, at least a quarter of the companies on the index are offshore players, either domiciled overseas or getting the bulk of their income from outside the Singapore economy.

The STI needs to be expanded to include a more broad-based set of companies that better reflect the diversity, vibrancy and complexity of the market. It also needs to reflect the Singapore economy, in some way.

One way might be to redistribute the weighting by expanding from 30 component companies to, say, 50 companies. It will surely be a broader representation of the Singapore bourse.

The STI is one of only two key indexes of the Singapore market (the other being the MSCI Singapore).

Many active fund managers track these indexes to compare their fund performances. Many also model their portfolios based on these indexes. So there is an imperative to ensure that the indexes accurately reflect the market's underlying performance.

The pandemic that has ravaged the world has changed economies, companies and investment priorities. Sectors covering tech, healthcare and supply-chain players have benefited where many other traditional businesses have suffered. Many of them will emerge as formidable players in a new emerging post-Covid-19 economy.

Global equity indexes, including the STI, must make adjustments to recognise and capture these changes. As it stands, the STI covers a very small segment of the local economy.

Indexes should be reviewed periodically to ensure that "mega trends" are sufficiently captured in them as far as possible, so that those looking to invest in these indexes through exchange-traded funds and even funds benchmarked to key indexes will not miss out on the new economy stocks that have taken the lead in the stock market's charge ahead in recent years.

As the manager of the Dow said, an index must identify businesses that better reflect the local economy and market.

As far as the STI goes, there are only two pertinent questions: Is it relevant and reflective of the Singapore market and economy? If not, what can be done to make it better?