SINGAPORE - Shares of Temasek-sponsored Vertex Technology Acquisition Corporation (VTAC), Singapore’s first special purpose acquisition company, or Spac, were suspended from trading on Nov 28, pending the outcome of an upcoming extraordinary general meeting (EGM).

A Spac, or blank-cheque company, is created to raise capital through an initial public offering (IPO) for the purpose of acquiring or merging with a private firm.

At the EGM at 2pm on Dec 1, shareholders of VTAC, which listed on the Singapore Exchange (SGX) in January 2022, will vote on the acquisition of live-streaming app 17Live.

An acquisition, if approved, could result in the SGX’s first pure-play Internet stock, 17Live Group, and could encourage others in the regional consumer tech sector to list here.

If investors buy 17Live’s growth story and are willing to bet that live-streaming will take off in South-east Asia, the listing of 17Live Group could also draw a more diverse base of investors to the SGX, adding vibrancy and liquidity to the local bourse.

Here are some things to know as shareholders prepare to vote.

Why was 17Live selected as an acquisition target? How does its business work?

In its IPO prospectus, VTAC stated that its aim is to identify a high-growth company with deep domain expertise in areas including consumer Internet and technologies. The company must be at an inflection point in its growth journey and ready to undertake an IPO.

VTAC is sponsored by Temasek-backed venture capital firm Vertex Venture Holdings.

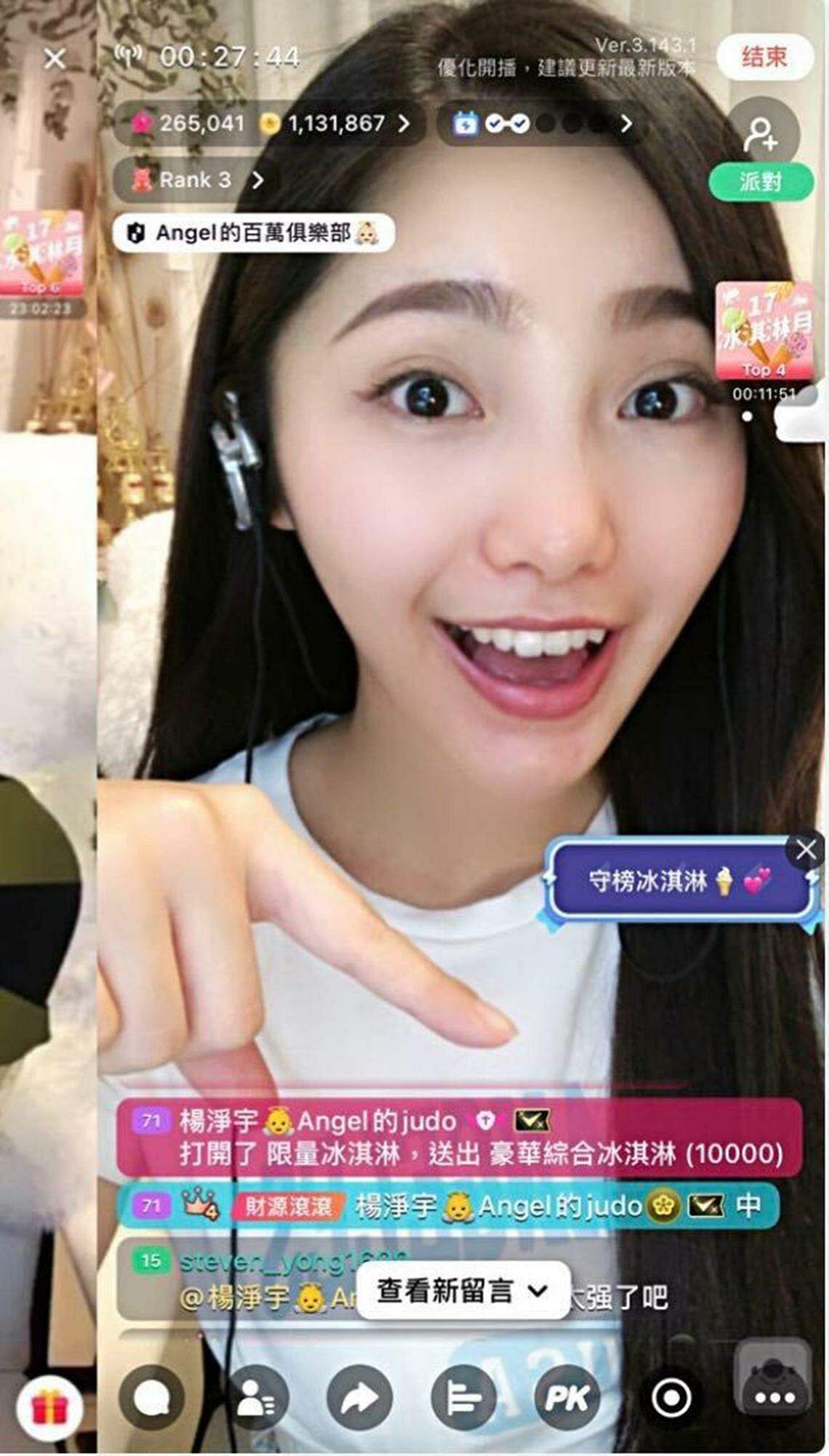

Live-streaming app 17Live was selected from Vertex’s portfolio of more than 300 companies. It owns the technology behind an Internet platform where aspiring individuals can sing, experiment with make-up and fashion, cook or play games, among other things, while interacting with their followers in real time.

One reason 17Live is viewed as unique is that it allows viewers to be engaged by and form emotional connections with their favourite streamers over the Internet. It enables communities to form among like-minded individuals and provides a convenient and affordable avenue of entertainment for a diverse user base.

17Live is the No.1 such platform in Japan and Taiwan, where live streaming is a growing business and part of the popular culture.

The app makes most of its money when viewers purchase virtual gifts for their preferred streamers in the app. The streamers then sell these virtual gifts back to the platform under a revenue-sharing model and based on a mutually agreed upon ratio.

To entice more users, 17Live organises several physical events a year, where streamers can compete for virtual votes and monetise their winnings. On Nov 20, it held its first such event live in Singapore.

17Live has exclusive contracts with 87,000 live streamers globally, and in the first half of 2023 recorded an average of 550,000 monthly users who spent around 93 minutes each day on the app.

What is the growth potential of 17Live? What are the risks?

Beyond Japan and Taiwan, 17Live wants to bring the culture of live streaming to Singapore and the rest of South-east Asia, where it sees untapped potential for growth.

Globally, the main growth driver is expected to be its V-Liver technology, which enables streamers to live-stream via an animated avatar on their mobile phones. In Japan, V-Liver has a 41.2 per cent projected average annual growth rate between 2023 and 2027, according to information provided by the company.

It also sees future growth coming from in-app gaming and live commerce.

There are risks to the acquisition though. For one, revenue has been easing since 2021 due to fewer active users and weaker average spending post-Covid-19, as well as a management decision to focus on profitability by targeting paying customers over scale.

For the first half of 2023, revenues totalled US$151 million (S$202 million), down by around 25 per cent from US$200.4 million during the same period a year ago. The company posted a loss of US$118.2 million for the first half compared to US$42 million a year ago.

However, after adjusting for the revaluation of its preferred shares and warrants, it recorded a profit of US$9.4 million. At the operating level, profit stood at US$15.8 million, up from US$4.3 million the year before.

Valuations also appear to be too high.

Research house Phillip Securities, in a Nov 20 report, placed a fair value of between US$581 million and US$700 million on 17Live. “When we equally weigh the importance of sales and earnings plus balance sheet strength, our 17Live fair value is US$641 million,” said Phillip Securities analyst Paul Chew.

In comparison, VTAC has proposed to acquire 17Live for Vertex Technology Acquisition Corporation for $800.8 million through the issuance of 162 million new shares. An additional 24.4 million earnout shares at $5 per share will be issued should 17Live meet specific financial targets, taking the potential acquisition value to a maximum of $922.8 million, or about US$691 million.

Assuming there is no redemption, VTAC’s assigned fair value as a combined entity would stand at $5.08 per share. However, it falls to a significantly lower fair value of $4.55 if the earnout shares are fully issued, Mr Chew said.

Shares of VTAC last traded at $4.79 before trading was suspended.

What are the transaction details and dates to watch out for?

VTAC shareholders who are not satisfied with the target acquisition have the option of redeeming their shares at $5 to $5.02 each and getting their initial investment capital back.

The last date and time to elect for redemption and submit the necessary forms is Nov 28. Under a bonus scheme from the company, non-redeeming shareholders are entitled to 0.1 free share for every share they own. Vertex Venture Holdings and Venezio, a vehicle of Temasek, will not be redeeming their shares.

An announcement on the level of redemptions and the outcome will be made during the EGM on Dec 1, and shares of VTAC will resume trading on Dec 4.

If shareholders vote in favour of the acquisition, shares of VTAC will begin trading under the new 17Live Group moniker on Dec 8.

Depending on the level of redemptions, the company is expected to have an equity value of between $996.9 million and $1.16 billion post completion.