SINGAPORE - Several changes to the Central Provident Fund (CPF), the national pension scheme here, will take place from 2025.

The Special Accounts (SA) of CPF members aged 55 and above will be closed, Deputy Prime Minister Lawrence Wong said in the Budget speech on Feb 16.

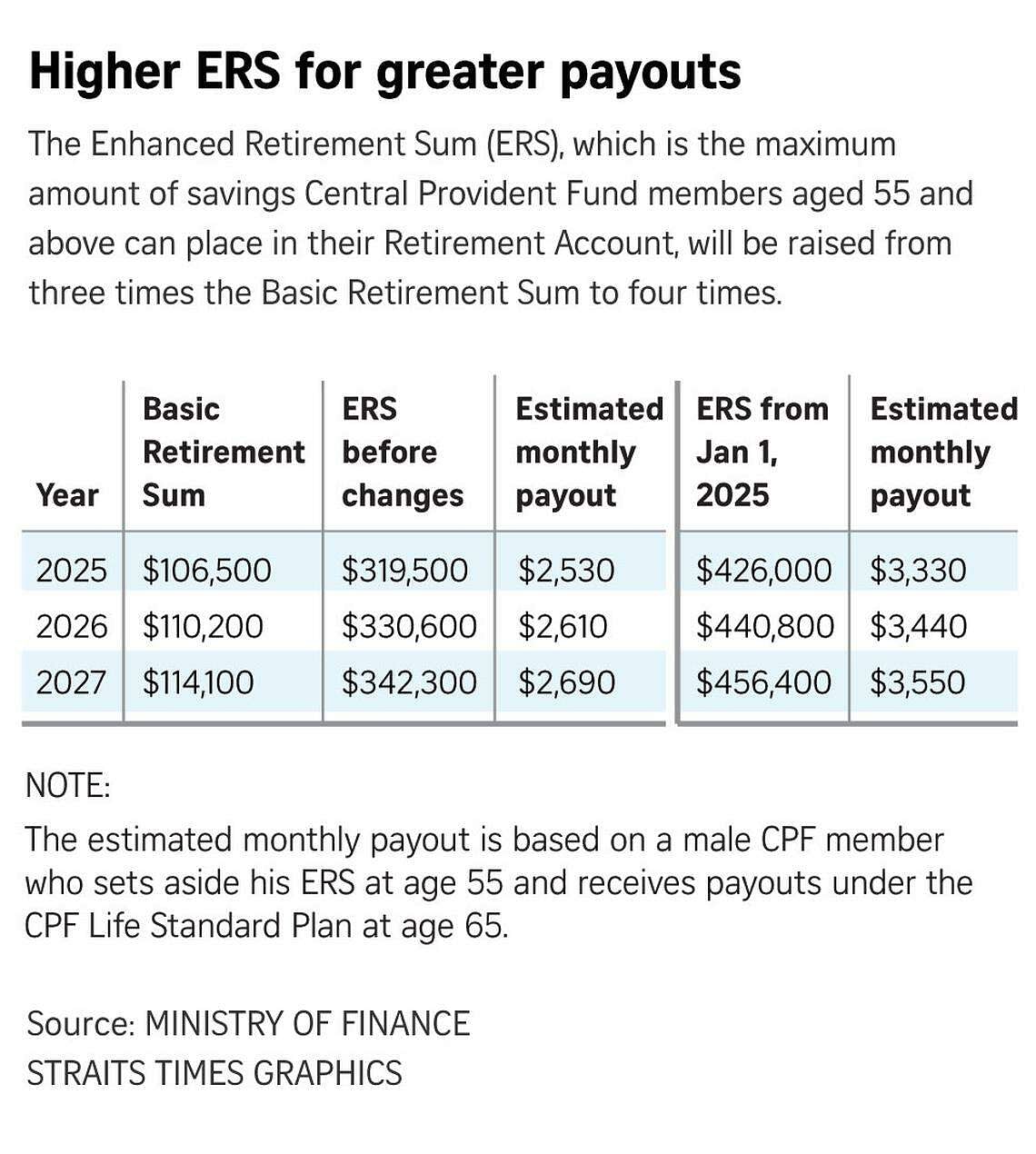

The Enhanced Retirement Sum (ERS), which is the maximum amount these members can commit towards CPF Life retirement payouts, will be raised to four times the Basic Retirement Sum (BRS), from three times currently. That means the ERS will be $426,000 in 2025.

The Enhanced, Full and Basic Retirement Sums are reference points for how much CPF members need to save to meet their desired monthly payouts.

The CPF Board said the reason for the closure of the SA is that some SA savings can be withdrawn from age 55, and savings that are withdrawable at any time should earn interest rates commensurate with their short-term nature.

The Straits Times answers questions on what the changes mean for CPF members.

1. How will the closure of the Special Account affect CPF members aged 55 and above?

A: On a CPF member’s 55th birthday, a Retirement Account (RA) is created for him. Currently, after the RA is created, the SA remains open, but that will no longer be the case from 2025.

When the SA is closed, the savings there will go into the RA up to the Full Retirement Sum (FRS) – which is two times the BRS, or $213,000 in 2025. Any savings beyond that will go into the Ordinary Account (OA), which offers a lower interest rate of 2.5 per cent per annum, compared with around 4 per cent for the SA and RA.

Any CPF contributions allocated to the SA currently – for example, if the CPF member is still working – will also go into the RA, up to the FRS.

People who may be affected are those who invest their SA savings through the CPF Investment Scheme to prevent them from being transferred to the RA at 55 – a practice known as Special Account “shielding”.

They typically do this within six months before they turn 55. After the RA is created, they liquidate their investments, keeping the funds in their SA to enjoy the withdrawal flexibility and higher interest rates.

With the closure of the SA, any proceeds from the investments if they are sold or reach maturity will be paid into the RA. Again, if the FRS in the RA is met, the monies will then go to the OA, where the interest rate is lower.

2. How can I continue to maximise the interest rates on my CPF balances after I turn 55?

A: If you have reached the FRS in your RA and have excess savings from the SA transferred to the OA, you can choose to move some of these savings into the RA up to the raised ERS to earn a higher interest rate.

These savings will earn at least the interest rate floor, which is currently 4 per cent, in your RA, but the transfer of savings to the RA cannot be reversed. These savings will be reserved to boost your retirement payouts and cannot be taken out for other purposes, such as investment or emergency needs.

So you have essentially given up the flexibility of being able to withdraw this money, which could have been sitting in your OA, in return for higher interest rates.

Only less than 1 per cent of the roughly 1.4 million CPF members – fewer than 10,000 CPF members – who are 55 and above today will not be able to transfer all the savings in their SA to their RA when their SA is closed in 2025.

This is because the savings in their SA and RA are already cumulatively more than the raised ERS, said the CPF Board.

The remaining 99 per cent of CPF members who are 55 and above today will be able to transfer all their SA savings to their RA up to the raised ERS.

The Straits Times understands that the detailed breakdown on how many people meet the various retirement sums will be revealed at the debate on the Ministry of Manpower’s budget in March.

Another option, if you want to be able to withdraw CPF savings any time, is to leave the money in the OA but earn a lower rate of 2.5 per cent per annum.

It is worth noting that members aged 55 and above earn a higher interest of up to 6 per cent per annum on the first $30,000 of combined balances in the OA and RA, capped at $20,000 for the OA. The next $30,000 of combined balances attracts interest of up to 5 per cent per annum, capped at $20,000 for the OA.

From 55, you can withdraw any remaining CPF balances once you have set aside the FRS in your RA, or the BRS if you own a property with a lease that can last you up to age 95 or older.

The latest data from the CPF Board shows that 69 per cent of CPF members who turned 65 in 2022 made lump-sum withdrawals before starting their CPF Life payouts at 65.

3. What does the increase in the ERS mean for CPF members aged 55 and above?

A: Savings in the RA go towards paying the premiums for CPF Life, the national annuity scheme.

The premiums currently earn interest of at least 4 per cent per annum. Premiums and interest compound over time and go towards giving the CPF member a monthly payout for the rest of his life.

The higher ERS means you have the option to commit more money to the CPF Life scheme in order to receive higher retirement payouts.

According to the CPF website, the raised ERS will be $426,000 in 2025, $440,800 in 2026, and $456,400 in 2027.

As an example, someone turning 55 in 2025 can get about $3,330 a month from CPF Life at age 65 if he chooses to save up to the raised ERS of $426,000. This is $800 more than the $2,530 or so he would receive with the current ERS of $319,500 for his cohort.

The above example assumes that the CPF member is on the CPF Life Standard Plan, which is one of three CPF Life payout plans.

The Standard Plan gives a steady monthly payout which does not increase over the years. The Escalating Plan gives lower monthly payouts initially. The payouts grow by 2 per cent a year for life and are aimed at keeping pace with inflation so that the member can maintain his desired retirement lifestyle even as the prices of items go up over the years.

The last plan, the Basic Plan, offers progressively lower payouts as one ages. This means the member will have to adjust his lifestyle and buy less in the future.

4. Will my take-home pay be affected?

A: Take-home pay will not be affected by the closure of the SA. The CPF balances are essentially being moved around the various accounts that a member has.

However, workers who are aged 55 up to 65 years old will have lower take-home pay due to a change in their CPF contribution rates. From January 2025, they will have to contribute 1 percentage point more to their CPF, as also announced in the Budget, and their employers will contribute 0.5 percentage point more, as also announced in the Budget.

The employee CPF contribution rate for workers aged above 55 up to 60 years old will go up to 17 per cent, while the contribution rate for those aged above 60 up to 65 will be raised to 11.5 per cent.

For example, a senior worker who is 56 and earns $2,000 monthly will have to contribute $340 to his CPF every month, up from $320 currently. His take-home pay will be $1,660 from January 2025, a drop of $20 from $1,680 currently.

Correction note: An earlier version of the story said that less than 1 per cent of CPF members, or roughly 14,000 people, will not be able to transfer all the savings in their SA to their RA when their SA is closed in 2025. The CPF Board has since clarified that fewer than 10,000 people will be affected.